Fill Out Your Cg 20 10 07 04 Liability Endorsement Template

The CG 20 10 07 04 Liability Endorsement form is a crucial document for businesses seeking to navigate the complexities of liability coverage. This endorsement specifically adds additional insured parties, such as owners, lessees, or contractors, to a commercial general liability policy. By doing so, it extends coverage to these entities for specific liabilities that may arise from the actions of the insured party. The endorsement outlines the conditions under which this additional coverage applies, primarily focusing on bodily injury, property damage, or personal and advertising injury linked to the insured's operations. It also emphasizes that the coverage is only effective to the extent permitted by law and must align with any contractual obligations. Importantly, the form includes specific exclusions, clarifying that coverage does not extend to incidents occurring after the completion of work or when the work has been put to its intended use. Furthermore, it sets limits on the amount payable on behalf of the additional insured, ensuring that it does not exceed the coverage required by contract or the policy limits. Understanding this endorsement is essential for both insured parties and additional insureds, as it delineates the boundaries of liability protection in various operational contexts.

Similar forms

The CG 20 10 07 04 Liability Endorsement form shares similarities with the Additional Insured Endorsement (CG 20 10). This document also extends coverage to additional insured parties, ensuring they are protected against liability for bodily injury, property damage, or personal and advertising injury. Like the CG 20 10 07 04, the CG 20 10 specifies that the additional insured status is granted only for claims arising from the named insured's operations. Both endorsements emphasize that the coverage provided is limited to what is required by contract, ensuring that the extent of protection aligns with the contractual obligations of the primary insured.

Another related document is the CG 20 33 Additional Insured – Owners, Lessees, or Contractors (Completed Operations). This endorsement is designed to cover additional insureds for liability arising from completed operations, which is particularly relevant in construction and contracting scenarios. Similar to the CG 20 10 07 04, it modifies the general liability policy to include protections for additional insureds but focuses specifically on claims that occur after the work has been completed. This distinction highlights the importance of understanding the timing of coverage and the specific nature of the operations involved.

The CG 20 37 Additional Insured – Designated Person or Organization endorsement is another document that aligns closely with the CG 20 10 07 04. This endorsement allows for the inclusion of specific individuals or organizations as additional insureds under the policy. Like the CG 20 10 07 04, it restricts coverage to liabilities arising from the named insured's work, ensuring that the additional insureds are only protected in connection with the operations specified in the endorsement. The focus on named individuals or organizations adds a layer of specificity that can be crucial for contractual relationships.

For those seeking to understand property transfers in Michigan, it's important to consider the legal tools available, such as the Michigan Quitclaim Deed, which can simplify this process. This form, used to convey real estate ownership without title guarantees, is essential for effective property transfers, especially when the seller wants to avoid warranty obligations. To start your journey with this important document, you can access additional resources, including templates like the one found at https://quitclaimdeedtemplate.com/michigan-quitclaim-deed-template.

The CG 20 26 Additional Insured – Blanket endorsement also bears similarities to the CG 20 10 07 04. This document provides broader coverage by automatically extending additional insured status to any party that the named insured is required to include under a written contract. The blanket nature of this endorsement allows for flexibility and ease of use in various contracting situations, much like the CG 20 10 07 04, which also limits the coverage based on contractual requirements. This ensures that both endorsements provide a tailored approach to risk management in business operations.

Lastly, the CG 20 11 Additional Insured – Managers or Lessors of Premises endorsement is relevant to the discussion. This document extends coverage to property managers or lessors, protecting them from liabilities that may arise while using the premises. Similar to the CG 20 10 07 04, it modifies the general liability policy to include additional insureds, but it focuses specifically on premises-related operations. Both endorsements require that the coverage aligns with contractual obligations, ensuring that the protections provided are consistent with the expectations set forth in agreements between parties.

Form Specifications

| Fact Name | Details |

|---|---|

| Policy Number | CG 20 10 12 19 |

| Purpose | This endorsement adds additional insured status to owners, lessees, or contractors for specific operations. |

| Coverage Limitations | Coverage applies only to the extent permitted by law and cannot exceed what is required by contract. |

| Exclusions | Bodily injury or property damage is not covered after the work is completed or when the work has been put to its intended use. |

| Insurance Limits | The maximum payout for additional insureds is the lesser of the contract requirement or the available insurance limits. |

Different PDF Templates

How to Create Payroll Checks - Each Payroll Check form aids in financial audits and reviews.

A Georgia Deed form is an essential document used to legally transfer property from one person to another. This form serves as evidence that the property owner has conveyed their interest in the property to the new owner. Completing this form correctly ensures that the transfer is recognized by law, securing the new owner's rights to the property. For additional details and resources, you can explore Georgia PDF Forms.

Designing a Family Crest - An identification tool used in nobility and royalty.

Roofing Estimate Example - Please provide your name for the roofing estimate request.

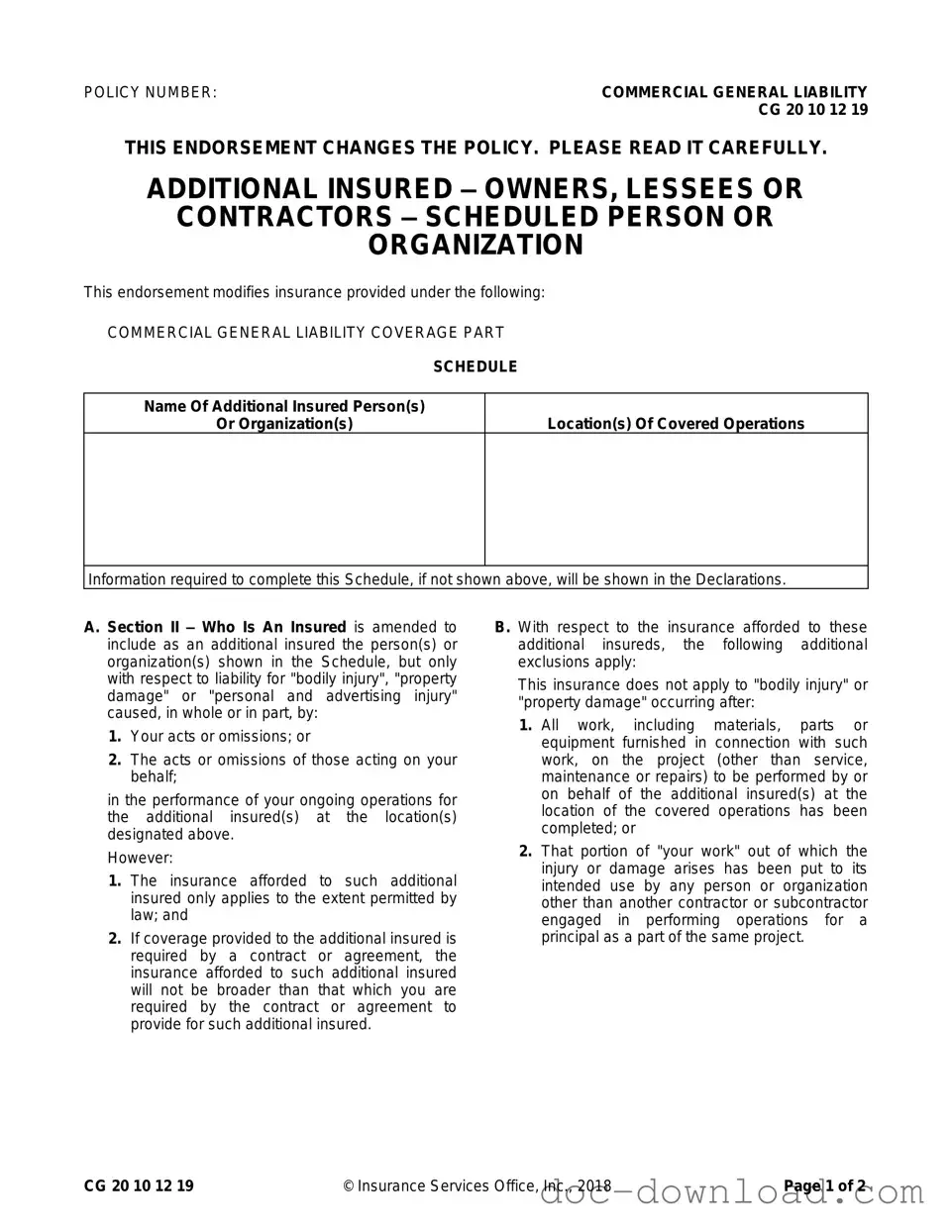

Sample - Cg 20 10 07 04 Liability Endorsement Form

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |